Global Growth Outlook: Modest and Uneven

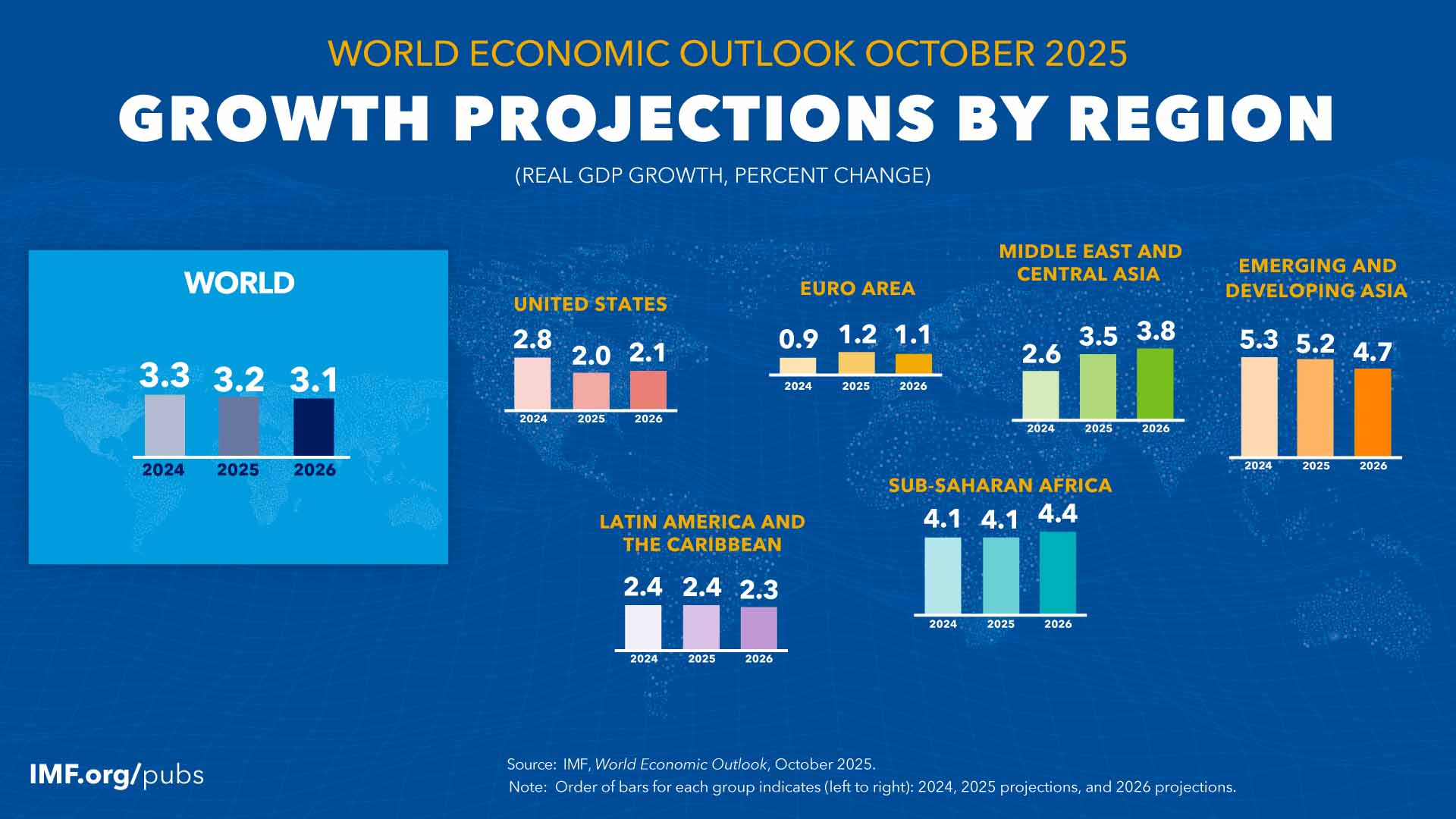

According to the latest International Monetary Fund (IMF) “World Economic Outlook: October 2025”, global growth is projected at 3.2% in 2025, up slightly from prior forecasts but still modest by historical standards. (Reuters) Advanced economies are expected to grow around 1.5%, while emerging markets may expand just above 4%. (IMF)

The IMF describes the environment as one of “flux” — growth is holding, but economic prospects are outweighed by uncertainty. (IMF)

Structural Shifts Redefining the Economic Game

A recent analysis by Commonwealth Bank of Australia highlights four structural forces reshaping the global economy: geopolitical fragmentation, the push to net zero, AI/technology, and demographic change. (CommBank)

This era heralds:

- Higher baseline interest rates due to diminished efficiency gains and elevated risk.

- Greater government intervention in strategic sectors (defence, tech, supply chains).

- Bifurcated markets, where segments diverge sharply between winners and losers.

Trade, Technology & Risk Factors

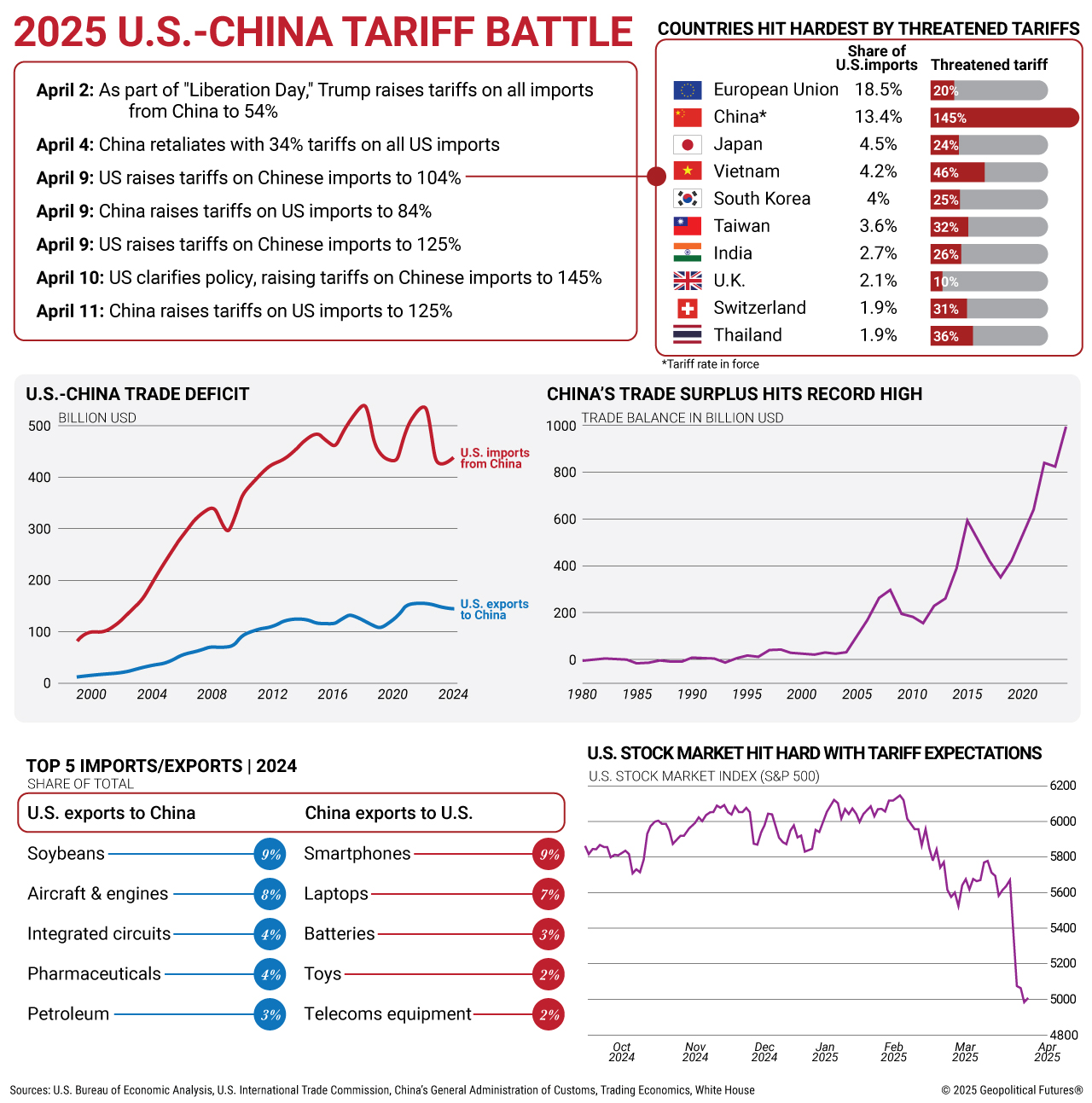

Trade tensions are re-emerging, most notably between the United States and China, with implications for manufacturing, supply chains, and investment flows. According to the World Trade Organization (WTO) & United Nations Conference on Trade and Development (UNCTAD) reports, global commercial services growth is forecast to slow to 4.6% in 2025 and 4.4% in 2026. (World Economic Forum)

A recent PMI bulletin from S&P Global shows the composite output index fell to 52.4 in September from 52.9, indicating expansion continues but momentum is waning. (S&P Global)

Regional Highlights

- United States: Economic momentum remains stronger than many peers, driven by investment in AI and technology. The IMF forecasts U.S. growth at about 2.0% for 2025. (Financial Times)

- Europe: Growth remains subdued. The European Department of the IMF warns that delayed reforms pose risks to future productivity. (IMF)

- Asia & Emerging Markets: While still growing faster than advanced economies, emerging markets face headwinds from trade and structural issues. India remains a bright spot. (The Economic Times)

Implications for Business & Investors

- Businesses should plan for modest growth, not boom conditions — focus on resilience, flexibility, and cost-control.

- Investors may need to temper expectations: equity markets may reflect optimism, but underlying growth remains constrained.

- Trade and technology strategies should be re-assessed: firms with international supply chains may face disruption or re-shoring pressures.

- Governments and firms must anticipate higher borrowing costs, longer cycles of investment payoff, and more active policy-shaping of industry.

Strategic Recommendations

- Diversify more broadly: Include both growth and defensive sectors; don’t rely solely on cyclical upside.

- Scenario-plan for volatility: Upside surprises are possible, but downside risks (trade shock, regulation, inflation) remain real.

- Monitor structural themes: AI, sustainability, and demographics continue to reshape competitive dynamics — align strategy accordingly.

- Enhance global agility: With fragmentation rising, being able to adapt to regional rule changes, tariff shifts and supply-chain shocks is vital.