By Hammad Yousaf

Published: November 3, 2025

Introduction

Multiple major global signals are flashing this week: manufacturing in Asia is contracting, the tech industry has seen another wave of layoffs, and the OPEC+ coalition has paused planned oil output increases for early 2026. Each of these moves on its own is noteworthy — together they paint a broader picture of shifting business, investment and trade-dynamics that readers of Market Financial Journal need to know.

Key Headlines

1. Asia’s factories hit by trade & tariff headwinds

In October 2025, major manufacturing economies in Asia registered weak factory activity amid renewed U.S. tariffs and weakening global demand. China’s factory activity slipped for the seventh consecutive month, and export orders to the U.S. plunged. (Reuters)

Why this matters: Asia’s export-led growth has long been a backbone for global supply chains. A slowdown signals risk for firms reliant on these flows and suggests upstream pressure on raw materials and component providers.

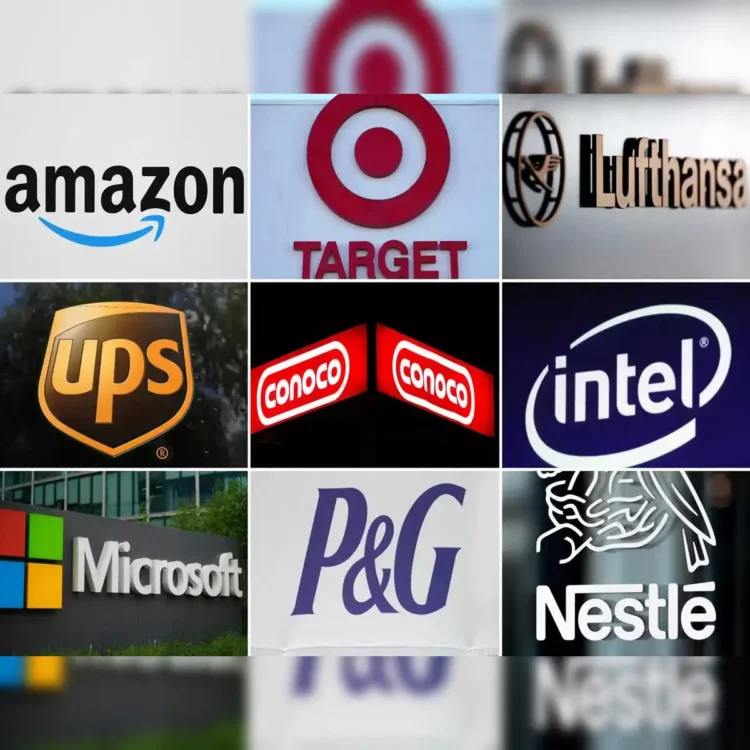

2. Tech industry jobs under increasing pressure

The global tech sector has seen over 100,000 job cuts so far in 2025 across more than 200 companies as firms pivot towards AI, cloud computing and greater efficiency. Major names like Amazon and Intel are leading the cuts. (Moneycontrol)

Why this matters: Tech has been a major driver of growth and investment. A pull-back signals caution, slower innovation adoption curves, and has wide consequences for employment, consumer demand and business services worldwide—including in the UK/USA.

3. OPEC+ to pause further oil output increases

The OPEC+ group announced it will pause any further increases in oil output through January-March 2026, warning of a possible oil glut and volatile market conditions. (Financial Times)

Why this matters: Oil is a key input for many industries. Supply decisions by OPEC+ affect global inflation, energy costs, and business investment. A pause signals caution on demand and has implications for energy-dependent sectors.

Implications for Business & Investors

- Supply chain risk rises: With Asian manufacturing cooling, companies should evaluate exposure to export slowdowns, component shortages or delayed production ramps.

- Capex and hiring will stay cautious: The tech layoffs and energy uncertainty suggest companies may delay major investments or scale support functions.

- Commodity & energy costs may moderate: A pause in oil output rises could ease cost pressures but also signal weaker demand ahead—meaning inflation might soften but growth could also taper.

- Investor sentiment may wobble: These signals combined increase risk of market volatility. Investors targeting UK/USA markets should lean towards firms with resilient models, diversified geographies and strong balance sheets.

Conclusion

The convergence of slower global manufacturing, major job cuts in tech and a cautious move by oil producers signals a business environment entering a phase of transition. Growth may remain steady, but with rising structural risks, firms and investors must stay nimble. At Market Financial Journal, we’ll keep tracking how these trends develop and impact markets in the UK, USA and globally.